The market is still talking about tungsten like this is just another metal chart.

It is not.

It is a permissions chart.

For years, the West treated tungsten dependence as a tolerable byproduct of globalization. China mined it, processed it, shipped it, and everyone else optimized around price. That looked efficient right up until export controls, tight inventories, and defense sourcing rules started moving upstream at the same time. Suddenly the question is no longer who can supply tungsten cheapest. The question is who can still supply tungsten that counts. (USGS 2026 tungsten chapter, Reuters on China’s February 2025 controls, Reuters on January 2026 record prices, DFARS restriction) (pubs.usgs.gov)

That is why I think Almonty matters.

Not because tungsten suddenly became important.

Because origin suddenly became important.

According to the USGS Mineral Commodity Summaries 2026 tungsten chapter, the United States has not mined tungsten commercially since 2015 and remained more than 50% net import reliant in 2025. The same USGS chapter puts 2025 world mine production at 85,000 tonnes, with China at 67,000 tonnes, or roughly 79% of global mine output. That is not a normal commodity setup. That is a concentrated system with very little margin for policy shocks. (pubs.usgs.gov)

Beijing made that vulnerability harder to ignore in February 2025, when it imposed export controls on selected tungsten items and required export licenses for affected products. Then, in January 2026, Reuters reported that tungsten prices hit record highs as inventories tightened, Chinese controls constrained overseas availability, and non-China supply remained limited. When a market is already this concentrated, those are not background headlines. They are the board changing shape in real time. (Reuters, Feb. 4 2025, Reuters, Jan. 29 2026) (Reuters)

And once the board changes, so does the payoff matrix.

In the old tungsten market, the rational buyer could wait. Why spend years rebuilding a non-China supply chain when material still flowed? Why fund redundancy before the shortage was obvious? Delay was comfortable.

In the new market, delay starts to look reckless.

That is because the compliance burden is moving upstream. Under the current DFARS rule and contract clause, the tungsten restriction tightens again on January 1, 2027: DoD contractors will no longer be able to acquire covered material that is mined, refined, separated, melted, or produced in a covered country. Once that deadline is in view, buyers are not just shopping for tungsten. They are shopping for compliant tungsten before everyone else reaches for the same pipe. (ecfr.gov)

That is the real Almonty story.

It is not mainly a bet on tungsten prices.

It is a bet on what happens when a neglected non-China asset goes from “nice to have” to “strategically necessary.”

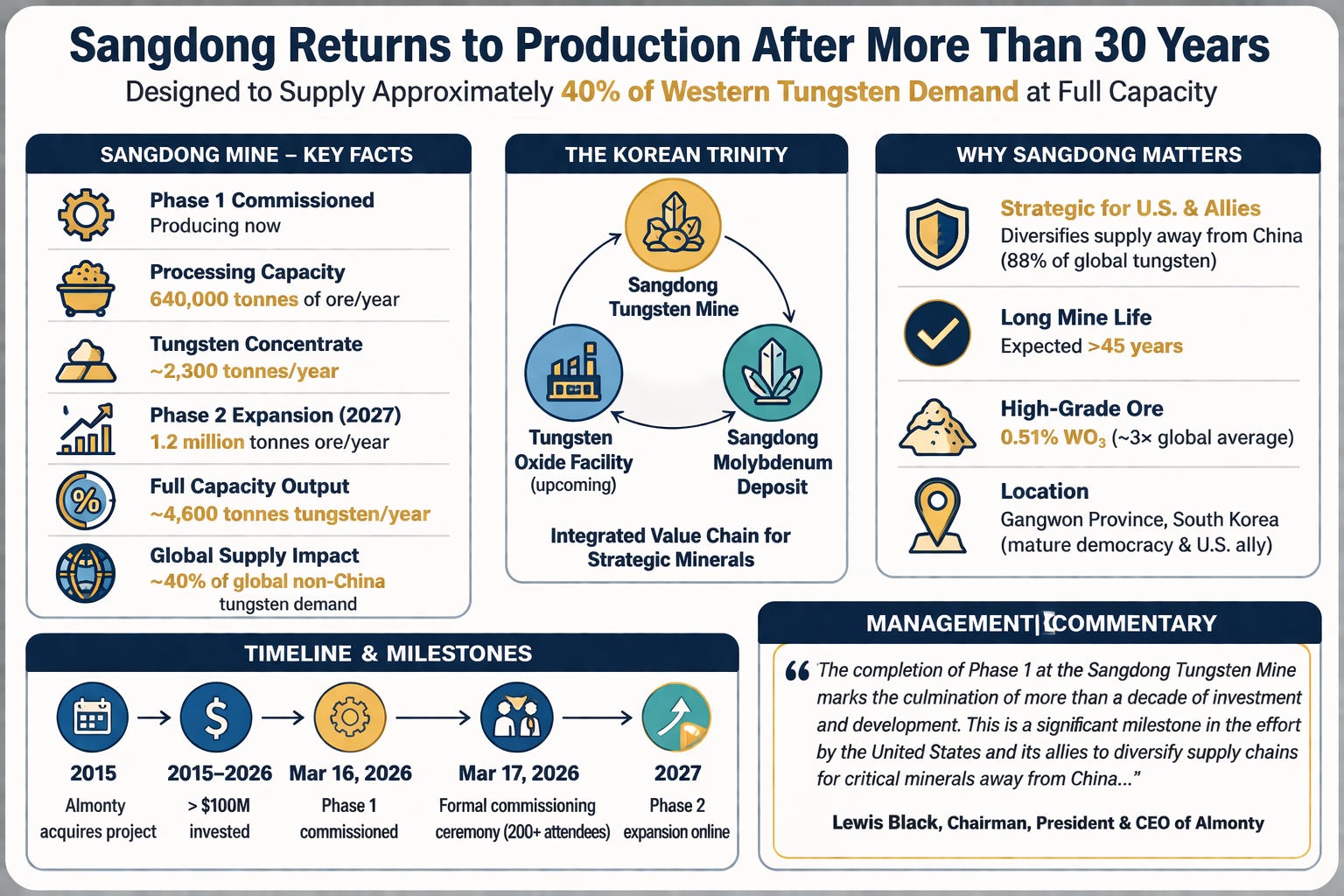

The turning point is Sangdong. On March 16, 2026, Almonty said it had completed Phase 1 commissioning at the Sangdong tungsten mine in South Korea, bringing the asset back into production after more than 30 years. Management says Phase 1 is designed to process about 640,000 tonnes of ore annually and yield roughly 2,300 tonnes of tungsten concentrate per year. A planned Phase 2, targeted for 2027, is designed to lift throughput to around 1.2 million tonnes of ore annually and roughly double output to about 4,600 tonnes of concentrate per year. Almonty also says Sangdong could supply around 40% of global tungsten demand outside China at full capacity. (Almonty Industries)

That matters because this is no longer a PowerPoint-only critical-minerals pitch.

The mine is commissioned.

The plant is producing.

The discussion has moved from “can this asset be built?” to “how quickly can it ramp, expand, and lock in strategic customers?”

The same March 16 release describes Sangdong as an asset with an expected mine life exceeding 45 years, an average ore grade of about 0.51% WO₃, and more than $100 million of redevelopment investment since Almonty acquired it in 2015. Those numbers matter because scarcity is one thing; scarce supply in the right jurisdiction, with real scale and long duration, is something else entirely. (Almonty Industries)

The financial side now looks more credible too. In its fourth-quarter and full-year 2025 results, released March 18, 2026, Almonty reported $32.5 million of revenue for full-year 2025, up 13% year over year. Year-end cash rose to $268.4 million from $7.8 million a year earlier, driven primarily by the July 2025 Nasdaq IPO and the December 2025 offering. Reported net loss was $161.9 million, but the company said the largest driver was an $87.3 million non-cash loss tied to the revaluation of embedded derivative liabilities after the share price appreciated sharply during the year. That does not make the story de-risked. It does mean the balance sheet now has real capacity behind the buildout. (Almonty Industries)

But the contract structure is what really makes this more than a simple tungsten beta trade.

In its SEC Form F-10 filing, Almonty says Sangdong is backed by a 15-year offtake agreement with Global Tungsten & Powders, part of the Plansee Group. The filing says the agreement covers 210,000 MTUs per year after ramp-up, which is more than 90% of expected Phase 1 output. It also says the agreement includes a floor price of US$183 per MTU based on an APT reference price of US$235 per MTU, with no upside cap, and that the material is exclusive to defense-only programs under U.S. Department of Defense guidelines. That is a very different economic profile from a miner that simply sells into the spot market and hopes the tape stays favorable.

The same SEC filing also says the project is supported by a US$75.1 million KfW IPEX-Bank financing facility, backed by the German state-owned KfW Group, with interest at SOFR + 2.3%. That matters because strategically important bottlenecks do not just attract higher prices. They attract financing structures that ordinary commodity stories rarely get.

Then there is the second layer: downstream control.

In a May 7, 2025 release, Almonty said Tungsten Parts Wyoming committed to purchase a minimum of 40 metric tons of tungsten oxide per month, with the material designated exclusively for U.S. defense applications including missile, drone, and ordnance systems. Almonty said deliveries would begin once it starts producing commercially saleable tungsten oxide, and that the agreement includes a hard floor price with no upside cap. That is important because the real choke point in critical materials is rarely just the rock. It is whether compliant material can move downstream without falling back into a China-dependent chain. (Almonty Industries)

That is also why the planned tungsten oxide facility matters. In the same SEC filing, Almonty says it is assessing a South Korean nano tungsten oxide plant with initial nameplate capacity of 4,000 tonnes per year, expandable to 6,000 tonnes, with operations targeted for 2028. The filing estimates capital cost at about €119.75 million, or roughly US$140.3 million, excluding remaining early-stage work and contingencies. That is where the thesis gets more interesting. The higher-value leverage in strategic materials usually sits further down the chain, where processing and origin rules start to matter more than simple mine output.

None of this makes Almonty risk-free.

Commercial ramp-up still has to work.

Phase 2 still has to be executed.

The oxide plant is still a plan, not an operating facility.

And Almonty’s own SEC filing is explicit that the tungsten oxide facility remains pre-construction, that operations are only targeted for 2028, and that financing, permitting, construction, and execution risks could all delay or prevent completion. The same filing also warns that slower-than-expected commercial production or cost overruns at Sangdong could damage the economics of the broader buildout. These are real risks. They just happen to be the risks attached to an asset that sits inside a strategically tightening supply chain.

That is why I think the better way to frame Almonty is not “leveraged tungsten exposure.”

That is too shallow.

The better framing is that Almonty is trying to become a listed vehicle for a non-China tungsten chain that can satisfy origin-sensitive, defense-sensitive demand before the rulebook tightens further. That is a more durable thesis than simply hoping commodity prices stay high. Commodity stories can collapse when pricing rolls over. Strategic bottleneck stories can keep pulling in capital and customer commitments because the buyer is not optimizing only for price anymore. The buyer is optimizing for resilience, compliance, and time. (Reuters)

More Articles

AI Won’t Kill SaaS. It Will Charge You Twice.

The old software model charged for employees. The new model charges for employees—and the AI agents doing part of their work.

The AI Trade Is Not a Bubble. It Is a Game of Chicken.

The question is not whether AI is real. The question is who gets paid — and who is only financing the table.

The Fed Did Not Move the Target. It Moved the Game.

FED chairman Warsh’s “different 2%” target is not about changing the number. It is about changing who gets to interpret it.