In Part I, the point was simple: the best setups are often the ones where spending is no longer optional. In Part II, the next layer was the metals themselves. This time, I want to go one step further upstream.

Because the game has changed.

We are no longer looking at one global supply chain optimizing for lowest cost. We are looking at multiple blocs optimizing for survivability. The U.S. is trying to organize a critical-minerals bloc, Japan and France just signed a rare-earths roadmap to cut China dependence, and France is now explicitly using resilience criteria to favor European supply in major renewable tenders. That is not theory. That is procurement.

And once the payoff matrix changes, the winners change with it.

In a fully globalized world, buyers mostly want the cheapest input. In a multipolar world, the dominant strategy becomes securing supply before someone else does. Governments stockpile. OEMs sign offtakes. Utilities lock in fuel. Buyers pay more for jurisdiction, redundancy, and political alignment. That is why this article is not just about good commodity exposure. It is about owning the resource positions that gain bargaining power when the world starts duplicating supply chains instead of sharing them.

For anyone following the series, I’m also tracking the portfolio of stocks discussed across these Bottleneck Trade articles on AI Trading Buddy, benchmarked against the S&P 500.

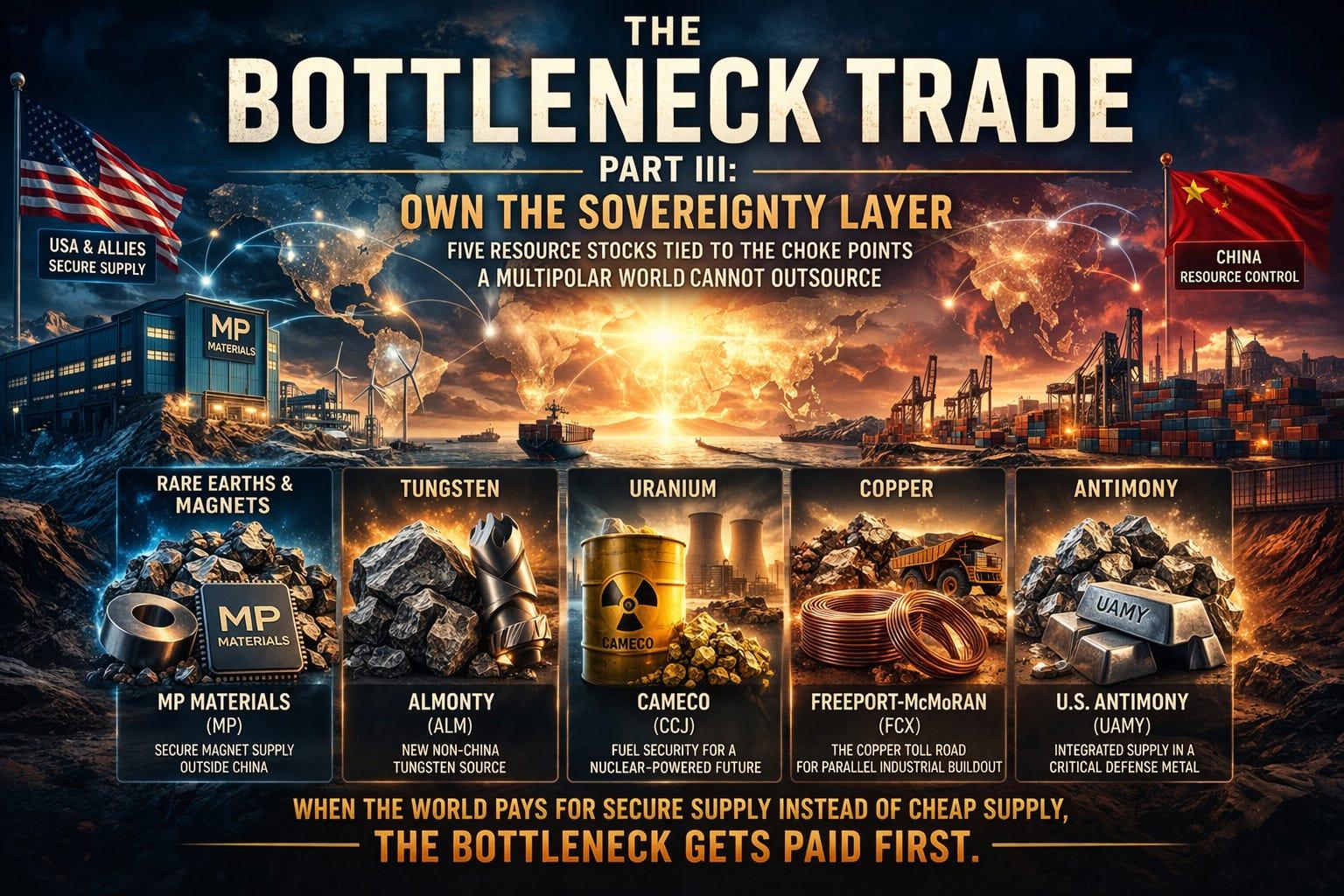

1) MP Materials (NYSE: MP)

Rare earths are still the cleanest sovereignty trade in the market.

USGS says global rare-earth mine production reached 390,000 tonnes in 2025, with China at 270,000 tonnes. That is still the core problem. The market talks a lot about diversification, but the world remains heavily dependent on a supplier that is willing to use export controls as leverage.

What makes MP the right stock here is that it has moved beyond the simple “mine in the ground” story. In 2025 the company produced a record 50,692 metric tons of REO in concentrate, a record 2,599 metric tons of NdPr oxide, signed a strategic offtake, and produced its first NdFeB magnets on commercial equipment. That matters because the real bottleneck in a fragmented world is not just ore. It is magnet-grade capacity inside allied jurisdictions.

If the market keeps moving from “cheap rare earths” to “secure magnets,” MP is still one of the few public names with real operating proof

2) Almonty Industries (Nasdaq: ALM)

Tungsten is one of those materials that matters more than its media profile suggests.

It sits behind tooling, hard metals, machining, and defense applications. In a globalized system, that usually means it stays ignored. In a fractured system, it suddenly becomes strategic because too much of the world still depends on China. USGS says China imposed new export controls on selected tungsten items in 2025 and prices surged sharply during the year.

Almonty is still the cleanest listed way to own that bottleneck, and the timing is much better now than it was a year ago. The company says Sangdong held a formal commissioning ceremony on March 17, 2026, marking the transition toward commercial operations. That takes it out of the “concept stock” bucket and into the much more interesting category: a strategically relevant non-China tungsten asset moving into the real world.

This is still a ramp story, so execution risk is obvious. But the logic is hard to ignore: every Western buyer has more incentive to back secure tungsten than to wait and hope China stays easy.

3) Cameco (NYSE: CCJ)

Uranium is no longer just a commodity call. It is increasingly a fuel-sovereignty call.

That matters because in a multipolar world, the objective is not just to have enough electricity. It is to have enough reliable electricity from a fuel chain your rivals do not control. The U.S. Department of Energy just committed $2.7 billion to rebuild domestic enrichment capacity over the next decade, explicitly to reduce dependence on foreign suppliers and strengthen LEU and HALEU supply.

Cameco is the right listed expression of that theme because it combines scale, operating proof, and fuel-cycle relevance. The company produced 21.0 million pounds of uranium in 2025, exceeded revised production guidance, and reported stronger annual results with contributions from uranium and Westinghouse.

That is a better fit for this article than a pure development uranium story. The bottleneck has moved from “find uranium somewhere” to “secure the upstream and midstream pieces of a politically reliable nuclear chain.” Cameco already sits inside that chain.

Positions from this analysis

-€139.39 total P/LMore Articles

The AI Trade Is Not a Bubble. It Is a Game of Chicken.

The question is not whether AI is real. The question is who gets paid — and who is only financing the table.

The Fed Did Not Move the Target. It Moved the Game.

FED chairman Warsh’s “different 2%” target is not about changing the number. It is about changing who gets to interpret it.

The Shiller P/E Is Screaming — And the IPO Market May Be Telling Us Who Is Selling

When valuations are near dot-com extremes and the IPO window reopens, stock pickers need to ask one uncomfortable question: are they buying future compounders — or someone else’s exit?